China National Petroleum Corporation, China Petrochemical Corporation, China National Offshore Oil Corporation, China National Energy Corporation, API, EU Network Certification Enterprise

13832731467

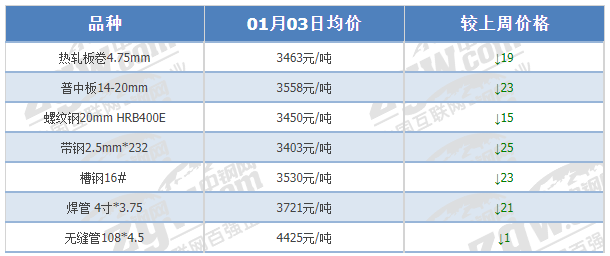

Inventory is currently available.Steel prices for major varieties saw a slight decline this week. As of January 3rd,Average Price of Rebar in Major Chinese Cities3450Yuan/tonDecreased by 15% from last week.Yuan per ton;Hot-Rolled CoilsAverage Price3463Yuan/TonDown 19% from last week.Yuan per ton;The average price of medium plate decreased by 23 yuan/ton to 3,558 yuan/ton, compared to last week; the average price of steel coil decreased by 25 yuan/ton to 3,403 yuan/ton; the prices of channel steel and welded pipe decreased by 23 and 21 yuan/ton, respectively, while the seamless tube price dropped by 1 yuan/ton from last week.

Overall,Although the stock market prices experienced a significant decline this week, the spot prices saw a smaller drop, mainly due to steel mills proactively controlling production.Partial varieties continue to experience specifications shortages.

According to the statistics from the China Steel Information Research Institute, from December 27 to January 3, due to the deep winter in the north, the rush to meet deadlines has largely ended. The overall prices of rebars in Handan, Beijing, and Hangzhou were relatively low, around 3,300 yuan/ton. The Wuhan area saw a slight increase, and the price gap between the north and south markets (compared to Guangzhou and Beijing) was about 170 yuan/ton.

Medium-thick plate prices in Handan, Zhengzhou, and Jinan saw significant declines, ranging from 60 to 80 yuan per ton. In the Wuhan area, prices increased by 10 yuan per ton. The price difference between the northern and southern markets (compared to Guangzhou and Handan) is around 340 yuan per ton.

As the year-end approaches, the general macro policies aimed at boosting economic development in 2025 have been sequentially released. However, their impact on the overall steel market is limited. The contradictions between supply and demand in the industry sector are becoming more pronounced, and support from the raw materials end is weakening. Market transactions are largely entering a "laid-back" phase. The weak start to this week's trading will continue to spread.YanmaWhat's the steel price trend next week?Let's dive right in!

Macro-levelGlobal concerns over economic stagnation and debt risks due to Trump's new administration policies have suppressed market sentiment. The probability of a Fed rate cut in January has decreased, which is bearish. Domestically, although favorable policies continue to exist, the short-term stimulus effect is not strong during the policy vacuum period.

In the industry sector,From the supply side, this week's pig iron production decreased by 267,000 tons to 2.252 million tons, the five major steel products production fell by 138.7 thousand tons to 8.2964 million tons, the total inventory increased by 63.7 thousand tons to 11.1574 million tons. The supply and demand remain weakly balanced, but the pressure of accumulating inventory has become prominent, which overall suppresses the rise in steel prices.

From the demand side perspective,On Friday, China's apparent demand for large steel products fell by 2.927 million tons to 8.2327 million tons, with continued decline in apparent demand largely in line with the off-season trend, further suppressing the rise in steel prices.

Material sourcing end,This weekIron ore productionSignificant DeclineMarket coking coal continues its downward trend, but the decline has narrowed.;Trade atmosphere in the imported Mongolian coal market slightly improves, coal pricesStableCoalNo Chinese content provided. Please provide the text to be translated.The valuation is currently lower for black, as soon as the downstream steel mills replenish their inventory during the later holiday season.No Chinese content provided, translation not applicable.Demand Initiated, PricingNo Chinese content provided.Stabilizing and halting the decline;But the time is not yet ripe, and the raw material sector remains weak in support.

Short-term macro benefits are limited, industry pressures are growing, raw material support is weak, and it is expected that steel prices will continue to fluctuate within a range and trend slightly weaker next week. Even with a short-term rebound, the height will still be limited.

Contact us

Service Hotline

13832731467

Company Telephone

13832731467

WeChat Number

13832731467

Address

32 Shigang Road, Cangzhou Economic Development Zone

www.114global.com © Zhongshang 114 Hebei Network Technology Co., Ltd.Address: Room 6009, Oriental New World Center, No.118 East Zhongshan Road, Qiaoxi District, Shijiazhuang City, Hebei ProvincePlatform Service Hotline: 4006299930